Are you ready to repay your student loans when the moratorium ends on August 31, 2022?

You’re already experiencing the economy’s pain with rising interest rates, high gas costs, expensive grocery bills, and record high rent and mortgage rates.

You’re nervous that President Biden might announce that he will not forgive student loan debt.

The question is, what should you do if your repayments begin on September 1st?

I’ve compiled a list of seven things you can do to repay your student loan debt. The best part is that it won’t add stress to your already stressful life.

Just a disclaimer, the following are for Federal Student Loans only. If you have a private student loan, speak with your loan provider.

Let’s figure out the best option to repay your student loan debt.

#1) Check Your Balance and Due Dates

If, for some reason, the student loan moratorium is suspended, you’ll receive your billing statement at least 21 days before your bill is due.

Unless you have consolidated your student loans, your interest rate should be the same as before the pause began.

You can check with your loan provider to determine your balance to begin factoring your student loans into your budget. But more on budgeting later.

#2) Deferment

A deferment allows you to pay no monthly payments over an agreed-upon time, with no interest. The government pays on your behalf monthly, so each payment counts towards your payment schedule.

Be mindful that not all Federal student loans are eligible for deferment, so be sure to discuss your particular loan with a student loan counselor to see if you qualify.

Common reasons to apply:

- You are undergoing cancer treatment

- You are experiencing economic hardship

- You have accepted a Graduate Fellowship

- You are attending school at least part-time

- You are active military or just completed active duty service

- You are a parent that took out a Parent-Plus loan

- You are undergoing rehabilitation training

- Or you are unemployed

One important thing to note is that you must continue making payments until your application is approved, so don’t apply and then jump ship.

#3) Forbearance

Like a deferment, forbearance temporarily allows you to cease payments on your principal; however, you are still responsible for paying back the interest.

Getting approval for forbearance is not automatic, so you must apply with your loan provider.

There are two types of Forbearance General and Mandatory.

Common reasons to apply for general forbearance is if you are unable to make your monthly payments due to:

- Financial difficulties

- Medical expenses

- Changing employment

- Or other reasons approved by your student loan provider

Mandatory forbearances must be granted if you apply if you are:

- In the Americorps

- You are in the Department of Defense

- You are currently in a Dental or Medical Internship or Residency

- You are in the National Guard

- You are experiencing a student loan burden, which means your loans make up more than 20% of your total monthly income.

One important thing to note is that if you put your loans into forbearance, I highly recommend at least paying the interest every month; otherwise, you will pay more on your loan in the end if you allow the interest to capitalize.

#4) Income-Driven Repayment Plans

There are four types of income-driven repayment plans:

- Revised Pay As You Earn Repayment Plan (REPAYE Plan)

- Pay As You Earn Repayment Plan (PAYE Plan)

- Income-Based Repayment Plan (IBR Plan)

- Income-Contingent Repayment Plan (ICR Plan)

Each plan has different eligibility requirements, and there is an application to gain approval. Contact your loan provider to see which plan best meets your needs. For more information, check out this list of student loan resources I’ve compiled.

“Under all four plans, any remaining loan balance is forgiven if your federal student loans aren’t fully repaid at the end of the repayment period.” ~studentaid.gov

With these plans, if you are working towards having your student loans forgiven through the Public Service Loan Forgiveness Program, you may qualify to have the remaining balance forgiven after ten years instead of the traditional 20 or 25 years.

#5) Autopay

Did you know that when you put your student loans on autopay that it saves you some interest?

I saved 0.25% monthly in interest while paying back my student loans. It may not seem like a lot, but over the life of the loan, it saved me a nice chunk of change.

Contact your provider to set it up if you’re ready to put your payments on autopay.

Note: It is highly recommended that you have a budget before putting your student loans on autopay to ensure that you will have sufficient funds.

#6) Bi-Weekly Payments

Do you know if your lender is calculating your interest rate using a simple daily interest formula or compound interest?

You can find out by calling your lender or visiting their FAQ page.

It’s important to understand whether you have a fixed or variable interest rate. Variable interest rates mean you will pay more if interest rates are higher than they currently are.

You can find your interest rate by contacting your lender or logging into your online portal.

After you know your interest rate and its calculation, you must verify your principal balance.

You can use the calculator found in this student loan repayment resource here to plug in your numbers.

The benefit of paying bi-weekly is that you will put more money towards your principal than the interest. Instead of paying 30 or 31 days of interest, you will only be paying 14 or 15 days.

#7) Add it to your budget.

If you already have a monthly budget, good for you.

You should know how much money is coming in and out of your account and how much you currently have leftover.

If your budget shows that you will have sufficient funds to include your student loan payments, I suggest putting your payments on autopay and/or using the bi-weekly payment.

Suppose your budget shows that you will have insufficient funds or that paying back your loans will be a financial hardship.

In that case, I suggest you apply for deferment or forbearance or see if you qualify for one of the four income-driven repayment plans.

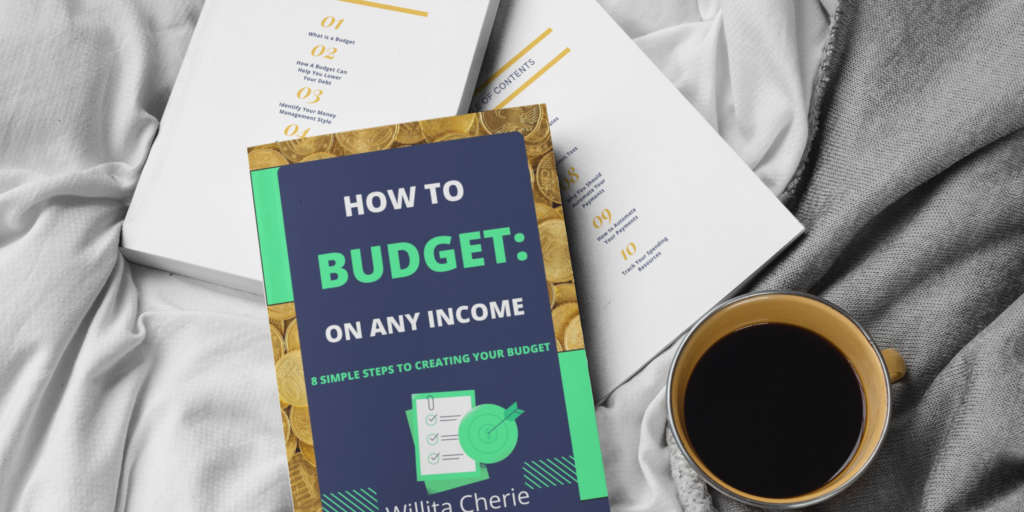

Additionally, you can buy a copy of my book How to Budget: On ANY Income here.

You Got This!

Imagine not sitting around waiting to find out bad news.

Imagine getting ahead of the crowd and making a preparation plan.

Preparation is key no matter if your student loan debt will be forgiven, paused, or need to be re-paid.

Waiting until the last minute to take action is irresponsible.

You have all the tools to make your student loan journey smooth.

Figure out which plan best suits your lifestyle and take action!

You don’t have to wait until President Biden makes his announcement to apply to the above recommendations; in fact, I highly suggest that you do so ASAP so that your application is ahead of the crowd, in the event you must resume payments on your student loans.

I hope this helped.

Here is the list of the resources that I mentioned in this blog:

- Student Loan Repayment Resource- https://buildyoung.willitacherie.com/repaymentplans

- How to Budget: On ANY Income- willitacherie.gumroad.com/l/budget

Let’s Stay Connected:

Subscribe to my Build Young Grow Wealthy Podcast (On Your Favorite Platform).

Here is the Apple Podcast Link:

Watch my Youtube Channel

Check out my website.